| Aspect | Traditional Shopping | Modern Shopping with BNPL |

| Payment Method | Upfront payment or credit/debit card. | Flexible payment plans (e.g., installments). |

| Approval Process | Credit card approval is required, which may involve lengthy paperwork. | Instant approval, often minimal documentation. |

| Purchase Flexibility | Full payment required at checkout. | Pay in installments over time (e.g., 4 payments). |

| Consumer Experience | One-time payment or credit card use at checkout. | Integrated BNPL options at checkout, often seamless. |

| Financial Impact | Immediate impact on cash flow. | Spread out cost, which can help manage cash flow. |

| Access to Credit | Based on credit history and card limits. | Less dependent on credit history, often no hard pull. |

| Interest Rates | Interest charges, if not paid off within the billing cycle. | Often, 0% interest for promotional periods. |

| Customer Service | Traditional credit card customer service. | Dedicated BNPL support teams, often responsive. |

| Transaction Speed | Typically fast but requires full payment upfront. | Quick checkout with the option to split payments. |

| Return and Refund Policies | Governed by store and credit card policies. | Can vary; often managed by BNPL provider and retailer. |

| Merchant Fees | Standard merchant fees for credit card transactions. | This may involve additional fees for BNPL providers. |

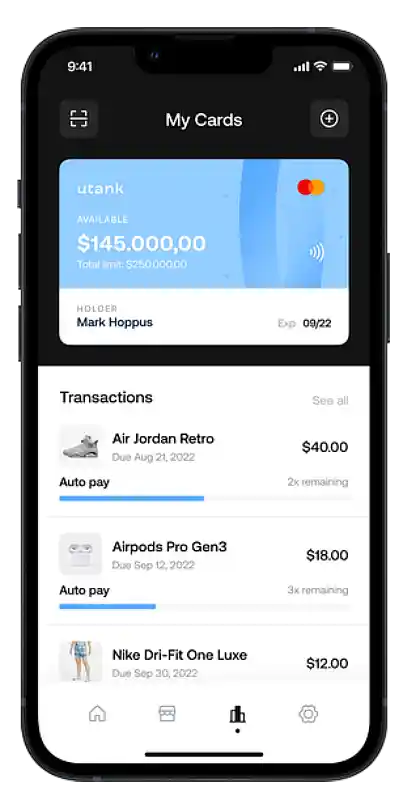

| Financial Tracking | Manual tracking or through credit card statements. | BNPL providers often offer app-based tracking. |

| Incentives and Offers | Rewards or discounts from credit card companies. | BNPL providers may offer promotional discounts. |